With the economy slowly gathering steam, the television business expects a brighter picture in the second half of the year.

There are good reasons for the rosier hue. Most of the fundamentals of the industry continue to point up. The advertising market improved as the upfront approached. Subscriber and retransmission fees continue to rise. And Netflix and other streaming video-on-demand players are supplementing the traditional syndication business.

Internationally, developing markets are creating opportunities for programmers, and improved business conditions in more mature markets are making contributions to the bottom lines of the major media companies.

The stock market has noticed. As the Dow Jones Industrial Average has risen, media stocks have skyrocketed, with many hitting all-time highs. Profits are fueling higher dividends and share buybacks, making the stocks even more attractive.

That said, there are reasons to temper the optimism. Advertising revenue growth is not what anyone would call robust. After a 2012-13 TV season in which their viewer numbers plummeted, the broadcast networks need to prove that they can still produce hits, starting with this fall’s schedule. The business model that generates huge margins for cable programmers is under pressure from online challengers and from à la carte advocates in Washington.

Meanwhile, technology and innovation marches on, and consumers can access video on more devices from more sources seemingly every day. In only some of these cases are programmers in control and able to cash in.

Here’s a closer look at some of the key factors affecting the TV business in the second half of 2013.

It’s The Economy, Stupid

Still coming back from the recession, media companies are finally operating with a more large-scale macroeconomy that has shrugged off potential land mines in the past year or so and could now be headed for smoother sailing.

“For the first time in a while, we’re heading into a summer without a fiscal cliff or a U.S. Treasury downgrade fear or concern that the next leg in the economy is materially down,” said David Bank, managing director of RBC Capital Markets. “I feel like there’s a pretty even-keeled view of the North American economy.”

“The economy is just gradually improving,” added Brian Wieser, senior research analyst at Pivotal Research Group. “Business has sort of shaken off the impact of the attempts at austerity, the payroll tax increase and other factors that could have retarded ad spending. It doesn’t seem like that’s going to be the case.”

Instead, the industry’s performance has been improving sequentially. “The year-to-year growth rates are looking better,” Wieser said.

At a recent investment conference, Viacom CEO Philippe Dauman said the economy looked to be strengthening for the next couple of years.

“We have a good dynamic going on right now. The macroeconomy is certainly recovering in the U.S.,” he said, adding, “Despite non-recovery yet in Continental Europe, we’re using this time period to build up our international scope with continued strategic and tactical realignment and development there.”

Better Days for Mad Men

The most economically sensitive part of the TV business is its advertising revenue. Vincent Letang, executive VP and director of global forecasting for media buyer Magna Global, said “We expect the economy [in the second] half to be better than the first.” Magna is predicting national TV ad revenue will be up 2% on a full-year basis, with growth in the second half between 2.8% and 3%.

Magna’s prediction is mostly based on economic forecasts, such as those published by the Federal Reserve Bank in Philadelphia. The statistics that correlate most closely to ad growth are personal consumption and industrial production, Letang said. This has not been a great year so far for industrial production, while personal consumption has been a bit more robust. Letang said he expects both metrics to accelerate in 2014, contributing to a 4% growth in national TV advertising dollars next year.

Till then, Magna sees broadcasters struggling in 2013, down 2% in revenue growth in the first half and down 1% in the second half for a total drop of 1.7%. Cable, meanwhile, is expected to grow 4.2%.

For the broadcasters, the problems predictably start with lower audience levels. “The big question is, is it just [last] season? Does it have something to do with the quality of the shows? Or is it the beginning of an acceleration of a real erosion of TV viewing among the youth?” Letang asked. “We think it might be a bit of both.”

Letang said that even though broadcast ratings are eroding faster than expected—and might have to be factored into Magna’s forecast in a few months—spending and revenue won’t fall nearly as far. “That’s the big paradox,” he said. “If there’s a reduction of supply and demand gets stronger, you’ll see an acceleration of inflation in prices on a cost-per-thousand-viewers [CPM] basis.”

RBC Capital Markets’ Bank said he would like to see a better performance from the shows the broadcasters put on the schedule during their upfront presentations in May. Bank added it’s important for CBS to demonstrate that it can continue to consistently generate the kind of high-quality content that drives the syndication model. For Fox, an improved primetime schedule is needed to stabilize the network’s advertising revenue, although broadcasting isn’t a big driver overall for News Corp., where the bulk of profits come from cable.

Technology: Friend or Foe?

The business of TV is experiencing unprecedented change from consumers using multiple devices to watch programming, and from new digital delivery systems.

Before the upfront presentations in May, a variety of Internet companies made NewFront pitches telling advertisers that more desirable consumers are getting entertainment, sports and news video via digital content. While online video programming is currently the fastestgrowing form of digital media, ad spending is expected to be $2.5 billion in 2013, according to Magna’s Letang, which is only 6.25% of the $40 billion spent on national television. “Even if the demand for online video doubles, it’s not going to change massively the outcome for conventional TV,” Letang said. That seems to be the case—for this year, at least.

Nevertheless, digital players—in addition to writing checks for off-network and library shows—are producing high-profile programming, such as Netflix’s resurrection of Fox’s Arrested Development, and starting to soak up viewers’ time.

If this has worried executives running more traditional businesses, they are not letting on. When Netflix let its deal to stream programming from Viacom expire, Viacom was able to find another buyer in Amazon.

“There’s never been a better time to be in the content business, at least for the next three or four years,” Discovery Communications CEO David Zaslav told an investors’ conference last month. “In the near term, what is happening here is very beneficial for us. A lot more people want to buy our content, [there are] new windows for our content, the U.S. is more pro"table than it’s ever been,” he said.

At the same time, Discovery is buying digital video companies, including Revision3. “People are spending time watching content on Netflix; they’re spending time watching content on YouTube. What does it all mean? We don’t really know what it means,” Zaslav said. “So on the left side of our company, we’re making our channels stronger, growing our market share, monetizing it, and we’re optimistic about that great model we have. On the right side, we’re saying let’s play around in this new space and see if we can get to know how people consume content and make sure that one of our brands is in front of them so we can learn from it and we can grow from it.”

Aereo in the Air

Other media companies are also looking for ways to exploit the growth in digital viewing. “We saw ABC roll out its Watch ABC [app]. I expect to see more of that in the second half,” said RBC’s Bank. “And I want to see how the Aereo lawsuits play out.”

Aereo, backed by former TV exec turned CEO of interactiveoriented IAC Barry Diller, has so far withstood legal challenges from the broadcast networks, which have sued claiming that Aereo is misappropriating its signal for its digital subscribers without paying retransmission fees the way cable operators do. “I’m less concerned about the ad market than I am about those kinds of things,” Bank said. “The content’s rich, the share shift in ratings, the technological and legal forces at play—these are things that are going to play out in the back half.”

One clue to how digital will play out will come when a buyer is found for Hulu, the video streaming website now being auctioned off by News Corp. and Walt Disney Co. (A third owner, Comcast, is a silent partner under terms of a consent decree issued when it acquired control of NBCUniversal.) Bank calls Hulu “the best brand in online television.”

Let’s Not Make a Deal

Other deals are in motion that could affect the way the second half of the year plays out. News Corp. is scheduled to split into two, separating its lagging publishing assets from its TV and movie businesses, which will be owned by a new public company controlled by Rupert Murdoch to be called 21th Century Fox. Those TV assets will be undergoing a fair amount of change. News Corp. also will be launching a new national sports channel, Fox Sports 1, a potential challenger to Disney’s dominant ESPN. It will be also launching FXX, the younger-skewing component of FX Networks.

Other potential deals are in the wind. Sony’s movie and television operations could go into play; the ever-growing Scripps Networks Interactive could finally complete a deal to acquire Tribune Co.’s stake in Food Network; and CBS has been accumulating cable programming assets. One of the bigger players could acquire one of the smaller players, further consolidating the industry.

“[On] the M&A landscape, one of these guys [might] do a big deal and we think it’s the wrong deal and our view of capital allocation could shift. That could be a driver in the wrong direction,” said Bank. “Our preferred capital allocation tends to be return of capital to shareholders. And I think a deviation from that, even for a good deal, could give some pause.”

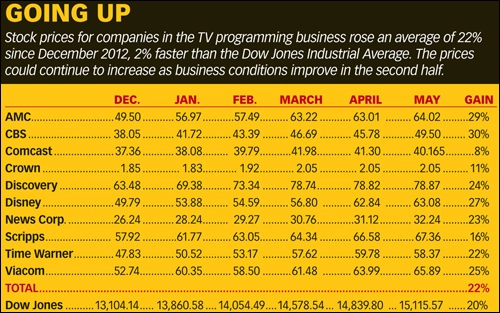

The Price Is Right

Wall Street likes the TV business. With the market rising in the first half of the year, media stocks rose even further. Could that rise continue?

One thing investors like about media stocks is that revenue has become fairly predictable, with affiliate fees and retransmission agreements being long-term and most ad sales locked in on a year-long basis.

“There’s so little that can change financial. Most ad spending is so pre-planned and share shifts take many, many years. It’s not likely we’ll see a rapid shift,” said Pivotal’s Wieser.

In the first half of the year, “the stock market performed really well, Wieser said. “It remains to be seen whether or not stocks can keep up. Underlying business performance will be OK with a pretty wide range of outcomes, depending on which company, which sector.”

In the last week the market, and media stocks in particular, pulled back. Todd Juenger of Sanford C. Bernstein said the decline was the result of selling by hedge funds and that there has not really been a significant change in business conditions, despite slightly lower than expected upfront price increases for the broadcast networks.

With the run-up of media stock in the past six months, some investors have been waiting for an opportunity to buy, and the current dip may give them a chance. Juenger specifically points to Discovery, which had the sharpest decline despite its earnings being revised upward. “The question now, for all those who said they wanted a better entry point, is: Will they still have the conviction to buy? We believe the ‘buy on the pullback’ case is very strong,” Juenger said.

E-mail comments to jlafayette@nbmedia.com and follow him on Twitter: @jlafayette