It seems like a simple solution. A $7 billion solution.

You have multichannel distributors complaining that they are under pressure from rising subscriber fees for cable channels—not to mention increasing retransmission rates from broadcast networks. At the same time, programmers say they need to pay for all of the additional original shows that can draw ratings at a time when viewers have more choices than ever.

There’s a recession on, so distributors say there’s a limit to how much they can charge customers before they cut the cord. Many programmers give lip service at least to the notion that they shouldn’t risk killing the golden goose that is the current pay-TV ecosystem, which produces billions of dollars in revenue and the high profit margin Wall Street craves.

The answer that has been emerging is for distributors to pay the channels that subscribers watch and cut back on the fees going to channels subscribers aren’t all that interested in. But that is easier said than done.

The most recent media company poobah to articulate this idea was Jeff Bewkes, CEO of Time Warner. Speaking last month at an investment conference in New York, Bewkes noted that it would be “stupid” to price “services everyone wants out of the reach of most of the people.” But like every programmer this side of ESPN, Bewkes said that his company’s networks now represent a mere fraction of distributors’ programming costs, and acknowledged that Time Warner plans “to have pretty aggressive wholesale revenue growth for our channels.”

How does the industry accomplish that? Bewkes pointed to what he called an interesting statistic. He said that distributors are currently paying $7 billion a year in fees to “marginal channels” outside of the top 40 in the ratings. Those channels, he said, account for only about 17% of viewing.

“What you’re going to see is basically a reallocation of the $7 billion of money going to failing channels into successful channels,” Bewkes said.

The argument would seem to be a good one, particularly for Time Warner, whose portfolio brims with networks that usually float near the top of the Nielsen ratings, including TNT and TBS, although its CNN has been struggling in prime time.

Other moguls also point out networks that are underpaid. Philippe Dauman, CEO of Viacom, claims his networks getting paid very little relative to the ratings they generate. News Corp. COO Chase Carey wants more for Fox News Channel. And now that it owns big networks, even Comcast’s Steve Burke says fees for top-rated USA Network should be higher.

And paying those high fees is easy, once those chubby, unwatched channels get cut, right? Well, maybe not.

“I think it is wishful thinking,” says Derek Baine, analyst at SNL Kagan who tracks the finances of the cable business. The good news is that when Baine runs the figures he finds that networks outside the top 40 in the ratings are pulling down closer to $8.5 billion in subscriber fees.

But the bad news is that “there are very, very few networks that are not linked to a major media company,” Baine says. “They are all bundled together so [operators] have to take the good with the bad. So in order to pay more [for the strong channels], you would have to drop a bunch of channels owned by Viacom, Discovery, News Corp. etc., which they are not going to let you do.”

Baine says that of the largest networks not in the top 10, few seem to be at risk of having their fees cut or being dropped by distributors, because they have powerful big brothers. Among them are ESPN2; NFL Network, which just signed an initial carriage deal with Time Warner Cable; a trio of Comcast channels—CNBC, Golf Channel and NBC Sports Network; Viacom’s VH1; Turner’s TCM; and three distributed by News Corp.—Big Ten Network, Speed and National Geographic Channel.

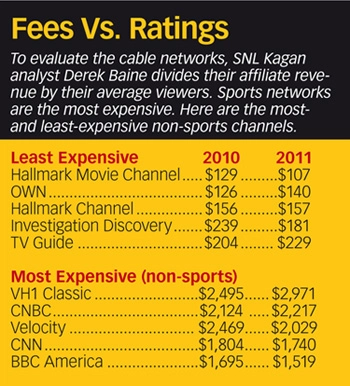

To gauge the relative value of networks, Baine takes their affiliate revenue and divides it by the average number of viewers. Even using this formula, most of the priciest nets are sports channels, led by ESPN at $7,368. Rounding out the top five costliest channels are NBC Sports Network, NBA-TV, NFL Network and MLB Network.

The average channel cost $580 in 2011 using this metric, up 13.9% from 2010.

Among the highest-priced non-sports networks relative to their ratings, most are owned by big programmers, including Viacom’s VH1 Classic; Comcast’s CNBC; Discovery Communications’ Velocity; CNN; and BBC America, distributed by Discovery. Other small, pricey networks include MSG Co.’s Fuse, Comcast’s Style and G4, News Corp.’s Nat Geo Wild; and Viacom’s Logo. Some of the potentially vulnerable independent channels were also among the cheapest, when divided by their ratings, limiting the savings operators could realize by cutting them. Those include Crown Media’s Hallmark and Hallmark Movie Channel and TV Guide Channel.

That’s not to say there aren’t some low-rated networks that might be worth cutting.

Fuse “definitely has gotten a lot of flak from operators,” Baine says. “That’s been reprogrammed a number of times and they just haven’t brought in the viewers.” Baine also notes that SoapNet has been a failure and that Walt Disney Co. is converting its subscribers to the new Disney Jr. Channel. Nat Geo Wild was launched out of the failed Fox Reality Channel and Style and G4 are relaunch candidates, according to Baine.

And while Logo is pricey, operators might think twice before dropping the only gay and lesbian-themed channel from their lineups, Baine adds.

E-mail comments to jlafayette@nbmedia.com and follow him on Twitter: @jlafayette